PART 2A OF FORM ADV – FIRM BROCHURE

Item 1: Cover Sheet

ClearList Capital LLC

625 6th Avenue, 3rd Floor

New York, New York 10011

Tel. 212-207-1370

www.clearlist.com

June 15, 2026

SEC File Number: 802-129459

CRD Number: 329206

This brochure provides information about the qualifications and business practices of ClearList Capital LLC (the “Adviser” or “ClearList Capital”). If you have any questions about the contents of this brochure, please contact us at 212.207.1370 or fundservices@clearlistcapital.com. Information in this brochure has not been approved or verified by the United States Securities and Exchange Commission (“SEC”) or by any state securities authority. Additional information about ClearList Capital is also available on the SEC’s website at www.adviserinfo.sec.gov.

REGISTRATION WITH THE SEC AS AN INVESTMENT ADVISER DOES NOT IMPLY THAT CLEARLIST CAPITAL OR ANY PRINCIPALS OR EMPLOYEES OF CLEARLIST CAPITAL POSSESS A PARTICULAR LEVEL OF SKILL OR TRAINING IN THE INVESTMENT ADVISORY OR ANY OTHER BUSINESS.

Item 2: Material Changes

Since the Adviser’s last filed brochure dated March 31, 2026, the Adviser has engaged an independent public auditing firm to conduct annual audits of its pooled investment vehicles. Item 13 of this Brochure has been updated accordingly.

The Adviser’s current and potential investors are encouraged to read this Brochure, as well as all of the governing documents applicable to their current or prospective investment, in their entirety. To receive a current copy of this brochure free of charge, please contact us at 212.207.1370 or fundservices@clearlistcapital.com.

Item 3: Table of Contents

Item 4: Advisory Business

Firm Description and Principal Owners

ClearList Capital LLC (herein the “Adviser”, “ClearList Capital”, “we” or “us”) operates as a Delaware Limited Liability Company in New York, New York and was established in October 2023.

The owner and sole member of ClearList Capital LLC is ClearList Holdings LLC, a limited liability company formed in Delaware in October 2019, detailed in Item 10 below. The Adviser is operated by its Executive Officers, including Patrick Murphy (Chief Executive Officer). ClearList Holdings LLC is owned by GTS Management Partners LLC (as Class A Member), and its control persons are the Class A Member, as well as David Lieberman and Ari Rubenstein.

The Adviser offers discretionary investment advice and management services to private investment funds (each, a “Client” and collectively, “Clients”), which are generally structured as limited liability companies. The term “private fund” means an issuer that would be an investment company, as defined in Section 3 of the Investment Company Act of 1940, but for Section 3(c)(1) or 3(c)(7) of that Act.

The Adviser serves as a fiduciary to its Clients, as defined under applicable laws and regulations. As a fiduciary, the Adviser upholds a duty of loyalty, fairness and good faith towards each Client, and as such is required to disclose all material conflicts of interest, and to mitigate potential conflicts of interest when possible. Our fiduciary commitment is further described in the Code of Ethics (see Item 11 – Code of Ethics, Participation or Interest in Client Transactions and Personal Trading for more information).

Investment Supervisory Services

We provide continuous advice and tailor our investment advisory services based on the individual needs of each Client. However, we do not tailor our advisory services to the individual needs of investors, and investors may not impose restrictions on investing in certain securities or types of investments.

We look for investments that meet the objectives, strategy and investment guidelines stated in each Client’s private placement memorandum, offering memorandum and/or operating agreement and other disclosures (collectively, the “Offering Documents”). We only recommend that a Client purchase a security when the Client’s stated objectives, strategy and investment guidelines are met in terms of the type of security and amount to be invested. We supervise the investment process and monitor the performance of each investment security held by our Clients. Please refer to the chart below for more information about each Client:

Fund Client

CLC AI LLC

CLC ALPHA LLC

CLRS X LLC

CLC X LLC

Manager

ClearList Capital LLC

ClearList Capital LLC

ClearList Capital LLC

ClearList Capital LLC

Carried Interest Member(s)

ClearList Securities GP, LLC

ClearList Securities GP, LLC and ClearRiver GP, LLC

ClearList Securities GP, LLC

ClearList Securities GP, LLC

We primarily target stock and equity securities in private companies (which may be formed as limited liability companies or limited partnerships). We also retain broad discretion to provide advicewith respect to a wide variety of securities in the future, including (i) any type of private or public stock or equity interests, (ii) investment company securities, (iii) warrants, (iv) debt securities, (v) municipal securities, (vi) options contracts on securities, (vii) various equity and debt interests in or secured by real estate, and (viii) interests in other investment funds such as private equity, real estate, buyout, venture capital and hedge funds.

While the Adviser has no subsidiaries, it is related to other businesses in the investment industry, including those referenced above (see Item 10 – Other Financial Industry Activities and Affiliations).

The Adviser does not operate any wrap fee programs.

The Adviser does not provide advice to clients that are retail investors.

As of December 31, 2025, the amount of RAUM with the Adviser, as defined by the SEC, was $959,804,083, all managed on a discretionary basis.

Item 5: Fees and Compensation

ClearList Capital is generally compensated for its services based on two types of fees: (i) a management fee assessed on total capital contributions and (ii) a performance fee paid to a related party as described in Item 6. Accounts initiated or terminated during a calendar quarter may be charged a prorated fee. Upon termination of any account, any prepaid, unearned fees will be promptly refunded, and any earned, unpaid fees will be due and payable. The exact terms of fees and expenses to be charged are set forth in the relevant Offering Documents of each Client. Investors and prospective investors must carefully review the Offering Documents of the Client in which they are invested or may invest, to review the specific fees and expenses applicable to their investment.

More specifically, the management fee (“Management Fee”) is paid monthly in advance to the Adviser. The amount of each Client’s Management Fee is disclosed in the respective Offering Documents. The Management Fee typically ranges from sixty basis points (0.6%) to two hundred basis points (2.0%) per annum of the aggregate capital contributions to the Client, variable among Classes. This fee will be shared with intermediary funds that certain Clients invest in and other affiliates and service providers, as applicable. To the extent that a Client has insufficient funds to pay Management Fees in full, the Adviser will accrue amounts owed. The Manager typically has the right, at its option and in its sole discretion, to decrease or waive the Management Fee applicable to certain members of each Client, and there may be a variance in fees charged to certain Clients and/or investors.

Please refer to Item 6 – Performance-Based Fees and Side-by-Side Management below for all information about carried interest, which is generally paid by each Client to a party or parties related to the Company when certain performance hurdles are met.

All fees are generally negotiable. The Adviser or an affiliate thereof, in their discretion, may waive or modify the Management Fee for certain large, strategic or other Investors. Please see Item 6 for important disclosures concerning side-by-side management. Additionally, the Adviser has entered and may enter into additional agreements, or “side letters” with investors, whereby such investors may be subject to terms and conditions that vary from or are more advantageous than those applicable to other investors.

Other Fees or Expenses

Other types of fees and expenses that are paid by a Client to either the Adviser or an affiliate are described in the Client’s Offering Documents.

Various operating expenses incidental to the provision of the day-to-day administrative services benefiting the Client, including its own overhead, are paid by the Client. Some of the other types of fees and expenses that are usually paid by a Client are: costs, expenses, and liabilities in connection with its organization and operations, including: organizational fees (i.e., formation fees, state filing fees and related fees, including legal expenses) and third-party administrator fees, referral fees or other fees of the Client and in addition to the Management and Referral fees (if applicable) described above, costs and expenses related to consummated and unconsummated investments, taxes, franchise taxes, securities and “blue sky” filing fees, banking and custody fees, fees and costs related to anti-money laundering and compliance, audits, accountants and counsel, and other extraordinary expenses. The Adviser reserves the right to charge each investor in a Client pro-rated portions of the Client’s estimated expenses in advance, which estimated amounts shall be reconciled against the Client’s actual expenses incurred during the Client’s term. Specific accounting procedures are further described in each Client’s operating agreement.

The Client may also reimburse the Adviser or an affiliate for the services performed by the Adviser’s attorneys and accounting personnel directly to or for the benefit of the Client (whether the services relate to general administrative matters or the business operations of the Client). These will be paid only if the Client would otherwise have engaged outside professionals to perform the services, and only if permitted to be charged based upon Client Offering Documents. These fees charged, if applicable, do not exceed rates customarily charged by outside attorneys or accounting professionals.

Although the Adviser has the right to collect a one-time referral fee from the Client (the “Referral Fee”) equal up to two hundred basis points (2.00%) of the aggregate capital contributions to the Client, such fee is only applicable to members referred by certain referral agents and, once collected, the fee is paid to the respective referral agent. The Referral Fee shall be allocated amongst the applicable investors in accordance with their relative interest in the Client. Offering Documents indicate when this fee is due, and when it applies. The Adviser reserves the right, at its option and in its sole discretion, to decrease or waive the Referral Fee applicable to certain investors of a Client without notice.

The Adviser is authorized by Clients to charge and deduct advisory fees directly from the assets of Clients. Specific information regarding our advisory fees, as well as other fees and expenses, can be found in the Offering Materials and/or operating agreement for each Fund Client.

Certain supervised persons of the Adviser accept compensation for the sale of securities or other investment products as registered representatives of certain affiliated broker-dealers. This may present a conflict of interest and gives the supervised person an incentive to recommend securities based on the compensation they receive. Please refer to Item 10 – Other Financial Industry Activities and Affiliations for further information.

Investors and prospective investors should refer to the applicable Offering Documents for a complete description of fees and expenses paid to the Adviser and its affiliates. The information contained herein is a summary only.

Item 6: Performance-Based Fees and Side-by-Side Management

Although the Adviser itself does not receive performance-based fees, affiliates serve as Carried Interest Member(s) of each Client (or their special-purpose related entities) and are entitled to receive a share of the profits generated from a Client, as these fees are disclosed to members/investors of each Client in the Offering Documents applicable to each Client. This share of profits is often referred to as a carried interest.

More specifically, Carried Interest Member(s) receive a performance-based fee ranging from 6.0% to 15.0% of distributions after investors have received 100% of their capital contributions back. This fee will be shared with intermediary funds that certain Clients invest in and other affiliates and service providers, as applicable. A full description of the entire fee arrangement is disclosed in the Client’s Offering Documents.

Clients and their investors who reside in the United States and who are charged performance fees or allocations are qualified clients as defined under the Investment Advisers Act of 1940, as amended (“Advisers Act”).

Since we are related to the Carried Interest Members of our Clients, carried interest earned when specific performance is achieved is considered performance-based compensation that indirectly benefits the Adviser. A carried interest may give the Adviser an incentive to take more risk or make more speculative investments in the absence of such a fee. In addition, the likelihood of earning a carried interest may give the Adviser an incentive to favor one Client over another in allocating investment opportunities or making buy, hold or sell recommendations. Lastly, cases where the Adviser manages the same investment made by two different Clients with potentially overlapping strategies (“side-by-side management”) may give rise to conflicts of interest such as potentially favoring one Client over another, particularly when it comes to allocating investment opportunities and allocating fees, expenses and resources.

The Adviser addresses the aforementioned potential conflicts of interest surrounding the receipt of performance-based fees and side-by-side management by recognizing its fiduciary duty owed to each Client, and reviewing each Client’s objective, strategy and investment guidelines alongside its recommendations and investment decisions. The Adviser has also adopted an allocation policy to manage these potential conflicts as needed.

Item 7: Types of Clients

ClearList Capital provides investment advisory services to private investment funds only, and references throughout this Brochure to “Clients” and to the Adviser’s related duties to and practices on behalf of its clients and/or investors should be construed accordingly. Please see Item 4 – Advisory Business above.

The Adviser’s Clients are private investment funds or other pooled investment vehicles formed under domestic laws and operated as investment pools that are excluded from the definition of an investment company under the Investment Company Act of 1940, as amended (the “Company Act”). The Adviser does not provide advice to “retail investors” as defined by Rule 204-5(d)(2) under the Advisers Act. Subject to certain qualifications, investors generally include individual investors, institutional investors, and other sophisticated investors; however, Client investors are not clients of the Adviser by virtue of their investment in a Client.

Each Client’s Offering Documents generally impose a minimum investment amount per investor; however, the Adviser may waive this minimum in their sole discretion.

Interests in the Clients at this time have been offered on a private placement basis, in reliance on Section 3(c)(7) of the Company Act, to persons who generally are “qualified purchasers” and “accredited investors” as defined under the SecuritiesAct of 1933, as amended (the “SecuritiesAct”), or “knowledgeable employees” as defined under the Company Act, and who are subject to certain other conditions, which are fully set forth in the Offering Documents of each Client. Interests in Clients may be offered to persons who are not “U.S. Persons,” as defined under Regulation S of the Securities Act, or who are tax-exempt U.S. Persons (or entities substantially comprised of tax-exempt U.S. Persons) and who are subject to certain other conditions, which are also set forth in each Client’s Offering Documents.

Item 8: Methods of Analysis, Investment Strategies and Risk of Loss

Methods of Analysis and Investment Strategies

The Adviser advises its Clients primarily about making investments in private companies that are often difficult to value. Each Client will have a specific strategy and investment focus that is described in the applicable Offering Documents. Some Clients may have strategies similar to other Clients. Offering Documents and/or operating agreements of Clients will include specific guidelines or restrictions on investments.

The Adviser’s objective is to:

- find investment opportunities that fit the Client’s specific strategy,

- diligently investigate each investment’s benefits and risks (called due diligence),

- make recommendations to each Client whether to buy, hold or sell an investment, and

- monitor the performance of investments made. The Adviser reviews its recommendations against any specific guidelines or restrictions on the Clients’ investments.

Due Diligence

Professional employees of the Adviser and/or its affiliates perform due diligence on each investment opportunity. Due diligence varies depending on the type of investment but typically includes some or all of the following:

- Review all organizational and offering documents

- Review and negotiation of relevant legal documents

- Review of available financial information

- Research and analysis of market information and competition

- Review and preparation/analysis of financial projections

- Background checks of key company management

- Review marketing documents

Risk of Loss

The types of securities we recommend to our Clients are illiquid and speculative. There is no guaranty that our recommendations will turn out to be profitable to our Clients or their investors. Our Clients may not be able to sell or liquidate recommended securities if our Clients need capital for other purposes. Our Clients generally do not offer redemption rights or other liquidity options to investors.

There are certain risk factorsthat apply generally to the types of investment securities we recommend to our Clients and are summarized below. There are also numerous risk factors that may apply to the specific investment program or strategy to be followed by a particular Client. These general and specific risks are described in the Offering Documents of each Client.

Illiquid Securities (High-Risk Investments): Clients are permitted to invest and may invest in high-risk investments in illiquid assets. Most Clients’ investments will be difficult to value. Return on investments is contingent on the cash flow, growth and prosperity of the portfolio company investments in which the Client invests. The success of these investments will be subject to factors over which the Client and the Adviser will have little or no control. Consequently, the Adviser’s investments are highly speculative.

Resale of portfolio company investments may be restricted by applicable securities and other laws, and there will generally be no public market for Clients’ portfolio investments. There can be no assurance that an interest in any Client will earn a return or that the returns on successful investments will be sufficient to permit return of capital or profits to the investors in any Client.

The Clients will invest in privately offered securities: Generally, very little public information exists about these opportunities, their historical operations and cash flows, and the Clients will be required to rely on the ability of the Adviser to obtain adequate information to evaluate the potential returns from investing in these opportunities. Moreover, these opportunities may rely on third-party managers and operators, and the loss of one or more of these individuals could have a significant impact on the investment returns from a particular Portfolio Investment.

Investments Through Intermediate Entities. Certain Clients will invest into intermediate entities that have themselves been formed for the purpose of investing in operating businesses. Such intermediate entities will typically charge their own management fees and expenses and generally receive a carried interest, in each case as set forth in the offering documents with respect to such investment. Accordingly, investors in Clients of the Adviser will, in these circumstances, be subject to an additional layer of fees and expenses, in addition to those payable to the Adviser and/or its affiliates.

In addition, such intermediate entities will have full discretion and control over the investments made into the underlying business. The managers of such intermediate entities may have additional interests, economic or otherwise, in the underlying portfolio company that may not align with the interests of the Client or the investors in the Client. The Client will hold an interest in the intermediate entity and not in the underlying operating company itself, and therefore will not appear on the cap table of the operating business, may not receive the same level of information rights, and will not benefit from any governance or minority protection rights typically negotiated by direct investors.

The Client will have little or no ability to influence the decisions of the intermediate entity, will be dependent upon the management of such entity to safeguard the investment, and will be subject to any regulatory, legal, tax, operational, and other risks borne by the intermediate entity. Further, there is no assurance that the reporting provided by the intermediate entity will be timely, comprehensive, or consistent with the information that would otherwise be available through a direct investment in the operating company. These factors may limit the Client’s ability to effectively monitor its investment, increase the risk of misalignment of interests, and reduce potential investment returns.

Investments in Distressed Assets: The Clients may make Portfolio Investments in ventures or assets that are experiencing financial distress. Such opportunities often involve an asset that is operating at a loss or with substantial variations in operating results from period to period. Portfolio Investments experiencing financial distress may be involved in insolvency proceedings and have the need for substantial additional capital to support continued operations or to improve their financial condition and may have very high amounts of leverage. Distressed investments may have further inability to service their debt obligations during an economic downturn or periods of rising interest rates, may not have access to more traditional methods of financing and may be unable to repay debt by refinancing. The value of distressed assets tend to be more volatile and may have increased price sensitivity to changing interest rates and adverse economic and business developments than other investment opportunities.

Distressed assets are often more sensitive to company-specific developments and changes in economic conditions than other investments.

Investment with Third Parties in Partnerships and Other Entities: The Clients may invest with third parties, including members of management, through consortiums of private equity investors, joint ventures, or other entities, thereby acquiring non-controlling interests in certain investments. Although the Clients may not have control over these investments and therefore may have a limited ability to protect its position therein, the Adviser expects that rights will be negotiated to protect the Clients’ interests.

Cybersecurity Breaches and Disruptions: Cybersecurity is a term that is used to describe the technology, processes and practices designed to protect networks, systems, computers, programs and data from cyber attacks and hacking as well as other damage or interruptions that, in either case, can result in damage and disruption to hardware and software systems, loss or corruption of data, or misappropriation of confidential or sensitive data.

The Adviser and its service providers depend on both outsourced and internal information technology systems to perform their functions. Despite the efforts with which we (as well as related parties and service providers) review their own information technology systems or those of our service providers, a party may not be in a position to verify the risk or reliability of such systems or to protect such systems.

Similarly, despite any training or other measures that the Adviser may perform with regard to its employees, professionals or any service providers, such individuals may intentionally or inadvertently take action or fail to act, in a manner that poses risks to the Adviser, its Clients and investors. Thus, the Clients, and their service providers may be subject to losses, and interruptions arising out of cyber incidents, phishing attempts, cybersecurity breaches, denial-of-service attacks, computer viruses, network failures, computer and telecommunication failures, employee and professional usage errors, power outages, and unauthorized access to computer networks and hardware and computer systems, in addition to catastrophic events, such as fires, hurricanes, floods and other natural disasters and terrorist incidents.

If Adviser hardware systems, networks or software are compromised, inoperable or stop functioning properly due to cyber related issues, it may result in significant cost to fix or replace them. The damage to, or interruption or failure of, these information technology systems for any reason could cause significant interruptions in our operations and result in a security breach, resulting in the loss of confidentiality or privacy of confidential or sensitive data, including personal information relating to investors, and cause material financial loss or harm. Such an occurrence could harm the Adviser or a Client’s reputation, subject any such entity and its respective affiliates to legal claims and otherwise affect its business and financial performance. Such damage to, or interruption or failure of, these information technology systems may cause losses to the Client by interfering with the operations of ClearList Capital or by requiring a significant amount of our resources.

Regulatory Risk: Statutes, regulations and policies are continually under review by the U.S. Congress and state legislatures and federal and state regulatory agencies. The introduction of new legislation or amendments to existing legislation and regulations (including changes in how they are interpreted or implemented) by governments and regulators, the decisions of courts and tribunals and the rulings and decisions of regulatory authorities, can adversely impact our Clients’ returns. The regulatory environment for private equity and private investment funds is evolving, and changes in the regulation of these funds and investments may adversely affect the value of investments held by the Clients, the cost of compliance with applicable regulations, and our ability to implement any business plan with respect to Clients and investments.

Investments in Securities and Other Assets Believed to Be Undervalued: The Adviser may invest assets in undervalued securities. The identification of such investment opportunities is a difficult task, and there are no assurances that such opportunities will be successfully recognized or acquired. While such investments offer opportunities for above-average capital appreciation, they also involve a high degree of financial risk and can result in substantial losses. Returns generated from such investments may not adequately compensate for the business and financial risks assumed. Such investments can sometimes include bonds and other fixed income securities, including, without limitation, commercial paper and “higher yielding” (and, therefore, higher risk) debt securities. It is likely that a major economic recession could severely disrupt the market for such investments and severely impact their value. In addition, it is likely that any such economic downturn could adversely affect the ability of the issuers of such obligations to repay principal and pay interest thereon and increase the incidence of default for such securities. Additionally, there can be no assurance that other investors will ever come to realize the value of some of these investments, and that they will ever increase in price. Furthermore, we may be forced to hold such investments for a substantial period of time before realizing their anticipated value.

Leverage: The Adviser may,subject to applicable regulations and restrictions, if any, outlined in Client Offering Documents, leverage Client’s capital. Using leverage usually results in a Client’s net assets increasing or decreasing at a greater rate than if borrowed money is not used to amplify the results of invested capital.

Other Instruments: ClearList Capital may use some or all of the investment strategies described above or other investment strategies in its discretion.

Please refer to the Client’s Offering Documents for specific and further information regarding methods of analysis of investment strategies and risk of loss specific to each Client.

Shared Restricted List: The Adviser and certain of its affiliated broker-dealers share restricted lists. As such, Clients will be restricted from acquiring or disposing of certain securities that are on the shared restricted lists. Please see Item 10 for more information.

Item 9: Disciplinary Information

Registered investment advisers are required to disclose all material facts regarding any legal or disciplinary events that would be material to an investor or potential investor’s evaluation of the adviser or the integrity of its management. The Adviser has not been involved in legal, regulatory or disciplinary events related to past or present Clients that would be material to the evaluation of the Adviser or the integrity of its management personnel.

Item 10: Other Financial Industry Activities and Affiliations

There are various financial industry businesses affiliated with the Adviser. The Adviser’s Clients and related parties associated with their structure are listed below. For specific information about the relationship or arrangements between these entities and conflicts of interest that are present, investors are directed to review specific information, along with relevant material risks, provided in Offering Documents for each Client.

Fund Client

CLC AI LLC

CLC ALPHA LLC

CLRS X LLC

CLC X LLC

Manager

ClearList Capital LLC

ClearList Capital LLC

ClearList Capital LLC

ClearList Capital LLC

Carried Interest Member(s)

ClearList Securities GP, LLC

ClearList Securities GP, LLC and ClearRiver GP, LLC

ClearList Securities GP, LLC

ClearList Securities GP, LLC

ClearList Holdings, LLC is Sole Member of ClearList Capital LLC

GTS Management Partners LLC is a Class A Member and owner of ClearList Holdings, LLC. Through this affiliation, the Adviser is related and/or under common control with other GTS businesses listed below.

Broker-Dealer Affiliations:

Patrick Murphy, the Chief Executive Officer of the Adviser, is a registered representative of ClearList Securities LLC, ClearList LLC and GTS Securities LLC, all SEC-registered broker-dealers and members of the Financial Industry Regulatory Authority (“FINRA”). Mr. Murphy also serves as the Managing Director, Head of NYSE Market Making and Listing Services of GTS Securities LLC, and CEO of ClearList LLC, ClearList Securities GP, LLC and ClearList Securities LLC. Kassidy Chaikin, the Chief Operating Officer of the Adviser, is a registered representative of ClearList Securities LLC and ClearList LLC. Ms. Chaikin also serves as the COO for ClearList LLC, ClearList Securities LLC and ClearList Securities GP LLC. Rick Gillette, the Chief Compliance Officer of the Adviser, is a registered representative of ClearList Securities LLC, ClearList LLC and GTS Securities LLC. Mr. Gillette also serves as the CCO and Associate General Counsel of GTS Securities LLC, and CCO of ClearList LLC and ClearList Securities LLC.

Please see below for additional information about the Adviser’s affiliated broker-dealers. ClearList Holdings, LLC is also the Sole Member of the following two broker-dealers:

- ClearList Securities LLC (CRD #309455/SEC #8-70540) – a broker-dealer primarily engaged in the private placement of securities.

- ClearList LLC (CRD #308066/SEC #8-70504) – a broker-dealer that manages an alternative trading system.

The Adviser is also related to the following broker-dealer businesses:

- GTS Securities LLC (CRD #149224/SEC #8-68126)

- GTS Execution Services, LLC (CRD #306364/SEC #8-70455)

The Adviser or the Clients have engaged ClearList Securities LLC to assist with placement of Client interests and/or sourcing investments for Clients for financial compensation. Any material conflicts arising from this relationship that are known at the time are disclosed in Offering Documents for each Client. In exchange for the aforementioned placement agent services, the Clients will pay fees which the Adviser views as reasonable in light of the services received and current industry rates. For the avoidance of doubt, any direct commissions payable to Mr. Murphy, Ms. Chaikin and Mr. Gillette with respect to any Client transaction will be disclosed to the Client’s investors. Aside from the compensation it will receive, ClearList Securities LLC will be incentivized to recommend investors to a Client because of Mr. Murphy,Ms. Chaikin and Mr. Gillette’s relationship with ClearList Securities LLC. The Adviser will comply with Rule 206(4)-1 of the Advisers Act with respect to any such engagement.

Please note that there are no material business arrangements or relationships between the Adviser, its Clients and ClearList LLC, GTS Securities LLC and GTS Execution Services, although the Adviser may share the same physical location or other resources including supervised persons/staff with these related parties.

At times, conflicts of interest will arise in allocating Mr. Murphy, Ms. Chaikin, Mr.Gillette and other supervised persons’ time and activity between the Adviser and the affiliated broker-dealers with which each of them are registered. However, they will continue to dedicate as much of their time and resources to the Adviser as is necessary and appropriate to meet the investment objectives of its Clients.

Please refer to the Offering Documents for a complete description of the fees, investment objectives, risks, conflicts of interest and other relevant information associated with investing in any Client. Persons affiliated with our firm may have investments in Clients and have an incentive to recommend investments in the Client over other investment opportunities.

Neither the Adviser nor any of its supervised persons are registered or have an application pending to register as a futures commission merchant, commodity pool operator, commodity trading advisor, or an associated person of the foregoing entities.

Item 11: Code of Ethics, Participation or Interest in Client Transactions & Personal Trading

The Adviser has adopted a Code of Ethics (the “Code”) that obligates the Adviser and its supervised persons to put the interests of the Clients before their own interests and to act honestly and fairly in all respects in their dealings with the Clients. All of the Adviser’s personnel are also required to comply with applicable federal securities laws. Upon onboarding with the Adviser and at least once a year thereafter, each supervised person is required to acknowledge their receipt and understanding of the Code and agree to be bound by it. Supervised persons are required to promptly report any violations of the Code of which they become aware. For additional information about the Code or to request a copy, please contact the Adviser at 212.207.1370 or fundservices@clearlistcapital.com.

The Code contains a securities trading policy, which sets forth standards of conduct that are expected of supervised persons, as well as addresses conflicts that can arise from personal trading. The Code covers standards of business conduct, prohibited business practices, personal trading requirements, reporting of personal securities transactions, insider trading, restrictions on accepting and giving significant gifts, and reporting of certain gifts and business entertainment items, among other items.

The Code includes a prohibition on insider trading and outlines strict policies that dictate how any such information is treated. Supervised persons are prohibited from trading, either personally or on behalf of others, in securities while in possession of MNPI regarding these securities or communicating MNPI to others. A restricted list is maintained regarding issuers for which the Adviser and certain affiliated broker-dealers

have MNPI.

In addition, supervised persons are required to submit quarterly reports of security transactions for their own accounts or any account in which they have a direct or indirect beneficial interest. The Adviser’s Code requires personnel to report their personal securities transactions and comply with the policies and procedures reasonably designed to prevent the misuse of, or trading upon, MNPI. In the course of its investment management and other activities, the Adviser will directly or indirectly come into possession of confidential or MNPI about issuers of securities, including issuers in which the Adviser or its related persons have invested or seek to invest on behalf of a Client. The Adviser is prohibited from improperly disclosing or using such information for its own benefit or for the benefit of any other person, including the Clients. The Adviser maintains written policies and procedures reasonably designed to prohibit the communication of such information to persons who do not have a legitimate need to know such information and to otherwise ensure that the Adviser is acting in compliance with applicable law. In certain circumstances, the Adviser will possess certain confidential or MNPI that, if disclosed, might be material to a decision to buy, sell or hold a security. The Adviser and its personnel are prohibited from communicating such information with respect to the Clients or using such information for the Clients’ benefit.

Participation or Interest in Client Transactions:

Supervised Persons of the Adviser will at times have interest in Clients’ transactions and positions personally or by virtue of their relationships with the Adviser’s affiliated broker-dealers. Such practices and relationships present a conflict where the Adviser or its related person is in a position to trade in a manner that could adversely affect the Clients. In addition to affecting the Adviser’s or its related persons’ objectivity, these practices by the Adviser or its related persons have the potential to also harm the Clients by adversely affecting the price at which the Client trades are executed. The Adviser has adopted the Code, in part, in an effort to minimize such conflicts. The Adviser requires its related persons to pre-clear certain transactions in their personal accounts with the Adviser’s Chief Compliance Officer or his delegate, who will deny permission to execute the transaction if the Adviser believes such transaction will have an adverse economic impact on the Client.

In addition, the Code prohibits the Adviser or its related persons from executing personal securities transactions of any kind in any securities on a restricted securities list maintained by the Chief Compliance Officer. All supervised persons of the Adviser are also required to provide broker confirmations of each transaction in which they engage and quarterly transaction reports. Trading in employee accounts will be reviewed by the Chief Compliance Officer or his delegate and reviewed against the restricted securities list. To the extent the Adviser buys or sells securities for a Client, at or about the same time that the Adviser or a related person buys or sells the same securities for their accounts, the Adviser and/or the related person, if and as applicable, will do so in accordance with the procedures described above in order to minimize the conflicts stemming from situations where the contemporaneous trading would result in an economic benefit for the Adviser or its related person to the detriment of a client.

From time to time, the Adviser will be presented with investment opportunities that would be suitable for more than one of the Clients. In determining which investment vehicles should participate in such investment opportunities, the Adviser and its affiliates are subject to conflicts of interest among the clients. The Adviser attempts to resolve these conflicts of interest in light of its obligations to Clients and attempts to allocate investment opportunities among investors in a fair and equitable manner and in accordance with the Adviser’s policies on investment allocation.

If a principal transaction or agency cross transaction arises, the Adviser will execute such transaction with the consent of the applicable Client or as otherwise permitted by Rule 206(3) of the Advisers Act. Client consent will be sought in connection with any approvals required under the Clients’ Offering Documents and the Advisers Act, including Rule 206(3) thereunder. Lastly, the Adviser has implemented policies and procedures to guard against any conflicts and risks that are enhanced by having supervised persons associated with multiple regulated entities at one time, including but not limited to conflicts of interest, misappropriation, proprietary or private information, and any other form of market manipulation.

Item 12: Brokerage Practices

As a general matter, the Adviser does not trade marketable securities, and therefore does not typically use broker-dealers to trade securities on the open market. To the extent the Adviser trades public securities, or will in the future trade securities that require us to select broker-dealers, we will do so in accordance with our best execution obligations. Best execution means the Adviser would take into account a range of factors in determining which broker to use for a particular transaction, including, among other things, (i) the ability of the broker to effect the transaction; (ii) transaction costs; (iii) the size and difficulty of the order; (iv) expertise in particular markets; and (v) the relative value of any research and brokerage services or products provided by such broker. This does not necessarily mean we would always solicit the lowest commission cost available. Rather, if we were to determine in good faith that the amount of commissions charged by a broker is reasonable in relation to the value of the research and brokerage products or services provided by such broker, we may pay commissions to such broker in an amount greater than the amount another broker may charge.

Aggregation of Trades: The Adviser does not aggregate the purchase or sale of securities for its Clients.

Item 13: Review of Accounts

Client investments are under continuous review by the Adviser. Such reviews include, but are not limited to, a review of existing investments, potential investments, cash availability, market fluctuations, significant events, and investment objectives. Reporting obligations to investors, if applicable, are outlined in the Offering Documents for each Client.

The Adviser has engaged an independent public accounting firm to conduct annual audits for each Client (See Item 15 – Custody below).

Item 14: Client Referrals and Other Compensation

The Adviser does not compensate any person for Client referrals.

The Adviser currently uses the services of affiliated and unaffiliated placement agents to offer interests to prospective investors, in accordance with Rule 206(4)-3 under the Advisers Act, where applicable. The Adviser, in return for a referral, will pay such placement agents a fee based upon the value of the referral’s investment into the relevant Client. All such arrangements with a placement agent are disclosed to relevant investors in the applicable Client’s Offering Documents. For additional information on fees, please refer to Item 5 – Fees and Compensation.

Item 15: Custody

Rule 206(4)-2 promulgated under the Investment Advisers Act of 1940, as amended (the “Custody Rule”) (and certain related rules and regulations under the Investment Advisers Act of 1940, as amended) imposes certain obligations on registered investment advisers that have custody or possession of any funds or securities in which any advisory client has any beneficial interest. An investment adviser is deemed to have custody or possession of client funds or securities if the adviser directly or indirectly holds client funds or securities or has the authority to obtain possession of them (regardless of whether the exercise of that authority or ability would be lawful).

ClearList is required to maintain the funds and securities (except for securities that meet the privately offered securities exemption in the Custody Rule) over which it has custody with a “qualified custodian.” Qualified custodians include banks, broker-dealers, futures commission merchants and certain foreign financial institutions.

Rule 206(4)-2 generally imposes on advisers with custody of clients’ funds or securities certain requirements concerning reports to such clients (including underlying investors in certain circumstances) and surprise examinations relating to such clients’ funds or securities. However, an adviser need not comply with such requirements with respect to its Clients that are pooled investment vehicles if the pooled investment vehicle: (i) is audited at least annually (and upon liquidation) by an independent public accountant that is registered with, and subject to regular inspection by the Public Company Accounting Oversight Board, and (ii) distributes its audited financial statements prepared in accordance with generally accepted accounting principles to the client, or, in certain circumstances, all limited partners, members or other beneficial owners, within 120 days of its fiscal year end.

ClearList intends to rely upon this exception for its pooled investment vehicle clients and therefore will be exempt from the Rule 206(4)-2 reporting and surprise examination requirements.

Item 16: Investment Discretion

The Adviser receives discretionary authority from the Client at the outset of an advisory relationship. In all cases, such discretion is to be exercised in a manner consistent with the stated investment objectives and restrictions for our Clients. The only limitations that may be placed on our investment discretion are those outlined in writing. Such limitations, if applicable, are included within the Client’s Offering Documents. These limitations may include exclusions of certain types of industries and/or countries.

Item 17: Voting Client Securities

The Adviser does not currently invest Client assets in public securities issuing proxies. In the event that we invest in publicly-held securities, we will accept authority to vote securities on behalf of Client investments, and ensure that such proxies are voted in the best interests of the Clients and in accordance with Rule 206(4)- 6.

Item 18: Financial Information

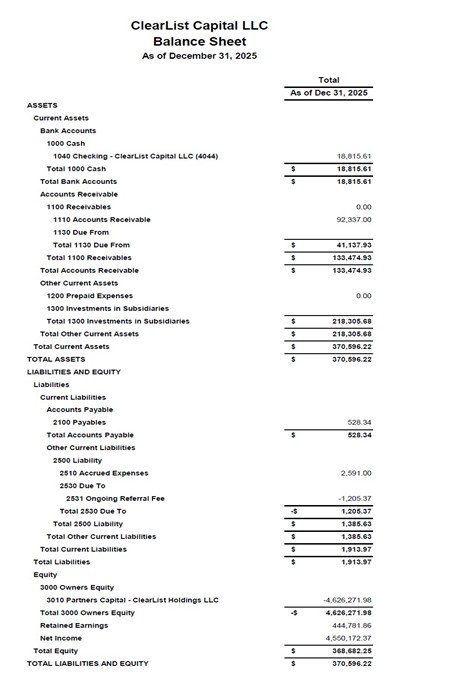

The Adviser requires the payment of more than $1,200 in fees six months or more in advance. As such, the Adviser has provided its balance sheet for its most recently completed fiscal year in Appendix A attached hereto.

The Adviser has no financial commitment(s) or conditions that are likely to impair its ability to meet contractual and fiduciary commitments to its Clients, nor has it ever been the subject of a bankruptcy proceeding.

APPENDIX A

CLEARLIST CAPITAL, LLC

BALANCE SHEET FOR FISCAL YEAR ENDING ON DECEMBER 31, 2025

This balance sheet has been prepared in accordance with generally accepted accounting principles (GAAP). Although it has not yet been audited by an independent public accountant, it reflects the Adviser’s financial position in accordance with GAAP. Investments reflect the Adviser’s proprietary investments in Clients made through its member, to the extent such investments represent the Adviser’s own assets.